Become a member & keep reading for free, or choose a paid membership.

Access all our content & email newsletter

We launched this site in mid July, so any ‘year in review’ articles are actually slightly misleading. When it comes to fundraising for midwest startups that is especially irksome as our analysis of these only started with Q2 2025 numbers and run through to a Q4 that isn’t even complete yet, at the time writing.

However, based on what the numbers in these stories tell us - and adding some info from the latest quarter - it should be no surprise that the story of fundraising for Midwest startups isn’t always a smooth, linear progression. Most especially when it comes to venture capital funding. This has never been more the case than this year.

In this region, we have a set of state-level ecosystems moving at different speeds, and subsequently we see totals that swing wildly based on a single deal or our own reporting decisions. As we said in our Q3 review: “progress here remains top-heavy and timing-sensitive.”

In any case, here is a compendium of what we published, what it implies, and what to watch out for in 2026.

1. The Midwest isn't boom v bust. It’s one-check v no-check.

If you want a simple framework for fundraising of Midwest startups and early-stage companies at any point in time, here it is: In most quarters, in most states, the difference between a ‘great’ quarter and a ‘grim’ one is a single later-stage check landing just inside the window so that it may be reported. In our Q3 round up we said “One big round at the right time can reframe an entire state’s narrative.”

This was most evident in Michigan in Q2, where the state posted a headline-grabbing $2.2B quarter. But the story immediately pivots to the fact that the financial backing provided to Grand Rapids Acrisure in the form of a $2.1B capital raise explained almost everything about that total. In fact, Q2 accounted for 75% of Michigan’s total and 27% of all funding for innovative ideas across the entire region for the year. Without this single injection of capital, the region would’ve actually experienced its lowest amount raised since 2017. Therefore this isn't a “Michigan is suddenly California” moment; it is a “single deal dwarfs the rest of the market” moment.

We saw a similar - if smaller - dynamic in Minnesota during Q3, where the state looked like the only ‘up and to the right’ story until you pulled at the thread: The $250m for FarmOp Capital’s growth equity round against a state total of $287m for the quarter. Strip the outlier out, and the picture changes fast.

And then there’s the other reality of the Midwest region, demonstrating that our entrepreneurial ecosystem is still in the earliest stages of development: even when a quarter isn’t dominated by one absurd outlier, it’s still often top-heavy.

- Michigan Q3: top five deals accounted for $133M of $141M.

- Ohio Q3: top five were ~65% of the quarter.

- Illinois Q3: top five were 78.7% of total.

- Indiana Q3: top five were $62M of $66.3M

So when people ask: “Is the Midwest underperforming?” our honest response is: Sometimes yes, sometimes no - but it’s always volatile, and almost always concentrated.

Additionally, if you only look at totals you might miss the signal. And the signal is usually how the numbers are actually distributed.

Related stories for further reading:

- Midwest Startup Fundraising – Q3 2025: Uneven, Outlier-Driven, and Sober

- Fundraising Q2, 2025: Michigan

- Minnesota Startups Funding: Q3 2025

2. Macro context and what to look for next year

In Q2 of this year the national market cooled. The number we cited: a 43% quarter-on-quarter national decline.

Then in Q3, national fundraising snapped back in a way that looked dramatic on paper, but was also top-heavy, driven by mega-rounds and concentrated in a handful of states.

That’s why our Q3 regional write-up landed on a simple conclusion: the progress of fundraising for Midwest startups remains timing-sensitive, and the previous quarter trend didn’t hold.

Now, as we close out 2025, here are the Q4-to-date totals with Q3 and YonY change in brackets:

- Illinois: $247M (-32% QoQ and -22% YoY)

- Indiana: $91.4M (+38% QoQ and -30% YoY)

- Michigan: $25.7M (-82% QoQ and -96% YoY)

- Minnesota: $440M (+53% QoQ and +57% YoY)

- Ohio: $111M (-67% QoQ and -59% YoY)

- Wisconsin: $18M (-43% QoQ and -85% YoY)

The short story: Ouch. Plus, Illinois has always been in a leadership position in our region. Is it still, based on these charts? and also, Minnesota local economy around health and life sciences is doing its thing… yet again.

Two important notes:

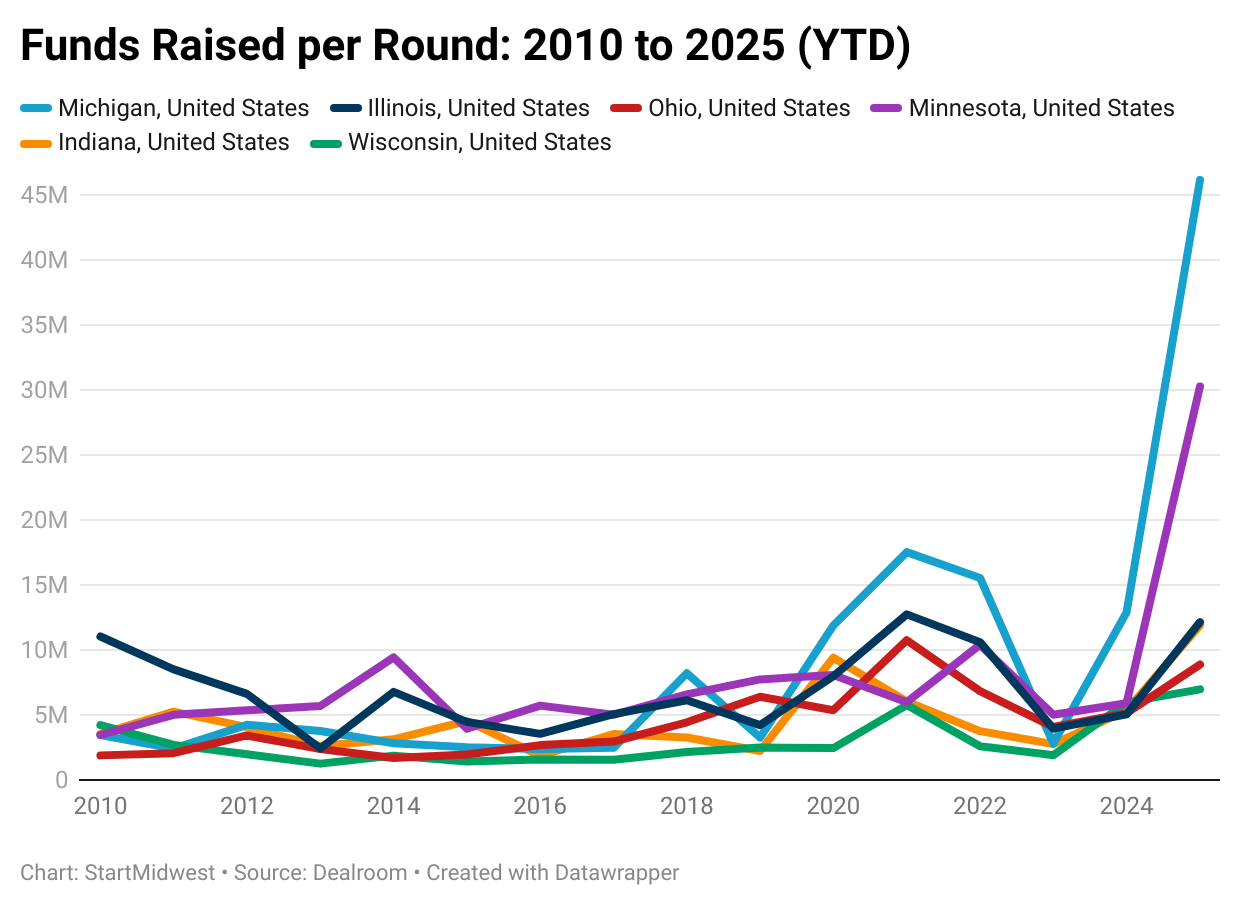

These are “to date” figures, and we’ll do the full accounting - state-by-state - in early January 2026, once reporting windows settle and the late announcements land. Until then, one thing that we’d like to point out are this year's figures when it comes to number of deals and value per deal. Rather than add comment, we’ll let the figures do the talking for themselves.

Firstly the number of deals for each year since 2010 (:

And Secondly, and more eye-wateringly… the funds raised per round by Midwest startups for each year since 2010:

We’re working on a larger “State of Midwest Tech” report that goes beyond quarterly totals into sector mix, ecosystem health, talent signals, and what actually drives compounding outcomes. If you want to learn more about partnering on that report then please get in touch.

3. State-by-state: maker states is too vague. The data isn’t.

One of the larger pieces we published this year was a decade-level lens looking at venture funds split by industry. The point of this was simple: if we’re going to talk about ‘Midwest solutions,’ we must consider our specific needs and which industries are actually getting funded and where that’s happening.

A few takeaways that may help you interpret each quarter:

- Illinois: probably the most diversified local economy in the region, with a comparatively even spread in the top three categories of its entrepreneurial ecosystem. That diversification shows up in how early-stage funding distributes over time, too.

- Minnesota: health and life sciences don't just lead - it’s structurally dominant in the state’s fundraising profile.

- Michigan: transportation dominates the decade-long view, but even there, outliers matter: the Lineage example is basically a case study in why quarterly charts swing.

- Ohio and Indiana: both look diversified in different ways, with innovative ideas in manufacturing appearing within the local economy even venture capital funding appears in other categories.

- Wisconsin: smaller totals make the state more sensitive to timing - and more likely to feel “quiet” even if there are breakthrough innovations happening.

The point isn’t to crown winners. It’s to stop treating the Midwest like one single blob. We know that, and we know that the region is a portfolio of ecosystems, each with its own “default settings.” Our goal though is to find or similarities so that we may push our stories forward collectively, while considering the differences.

4. How to read the numbers without lying to yourself

We’re going to keep saying this, because it’s the difference between insight and cope.

Data sources are imperfect. Category math is messy

In our industry-by-state analysis, we call out a key caveat: companies can appear in more than one category in Dealroom, which can replicate dollars. The estimate in that piece was ~5% repetition, and the guidance was clear: treat the figures as signals, not absolutes.

Timing changes headlines

Wisconsin Q3 is the clearest example of this. We wrote about the reporting conundrum explicitly: whether to place a round in Q2 (when it occurred) or Q3 (when it was announced), and how that decision meaningfully changes the story.

HQ vs roots matter: modern business is never clear cut

Ohio Q2 included a very Midwest-specific problem: the “is it still ours?” question when Midwest companies open a coastal HQ but is considered one of local startups with deep Cincinnati roots - and how we make those calls for our stories.

We count what credible data sources count, even when it sparks debate

Michigan Q3 addressed this head-on: whether large structured financings should count. Our stance was: if reputable aggregators report the dollars, we report the dollars - because those dollars still fuel teams, jobs, and outcomes.

Fundraising is slower, scrutiny is higher, liquidity still isn’t fully back

Our Invest360 panel recap put real voice to what founders feel: fewer rounds, tighter criteria, longer timelines, and investors waiting for liquidity to return. The piece cites Carta data and commentary around new investments on tightened expectations (profitability paths, retention, runway).

What’s next

In early 2026, we’ll be publishing a complete year-end review for each state covering Q1 to Q4 and a regional wrap, once Q4 numbers are finalized.

And beyond that: we’ll build the “State of Midwest Tech” report to go deeper than totals and into what actually compounds over time.

Because “how much did we raise?” is a useful question.

But on our pages and in this part of the world it has never been the most important one.

Trending Stories

All Rights Reserved

Copyright 2026 Zeroto7 LLC

Powered by: