Opinion

April 30, 2026

The Secret VC: Funds are the entry fee of Venture Capital. The Real Value is Reputation.

The Secret VC

Become a member & keep reading for free, or choose a paid membership.

Access all our content & email newsletter

Earlier this year, a founder I know came close to torpedoing their own round over a valuation cap disagreement. We weren't involved in the deal, but I became aware of it through the ‘back channels’ I’ve mentioned here previously. The back-and-forth apparently got close enough to the edge that it stuck with me, and a colleague and I ended up discussing it for the better part of an evening not long after.

The part that didn't add up wasn't the founder fighting for the survival of their company. After all, when the round closed they still owned the vast majority of the company’s shares and the valuation was more than respectable for his stage. The Investors involved in the deal have great reputations in the region and many were offering more than just capital, with great program support, network access for potential customers and more. But the founder was hemming and hawing over a few percentage points as if the cap table was the only line item that mattered in the equation.

What I want to talk about here isn’t the percentages, those were fine. The less comprehensible part - to me at least - was that the founder treated this relationship like a transaction and nothing more, and almost paid the price for it.

Dollars in Venture Capital are Basic, the Rest is not.

What many founders don’t realize is that money is actually the simplest thing in the room. Capital is easy to model, easy to compare across term sheets, easy to explain to co-founders. But when a deal gets uncomfortable, founders default to arguing about the variables they understand. They fight over percentages because they know how percentages work. Trust, conviction, alignment, reputation - those are more difficult to measure and nearly impossible to predict. They don't fit neatly into a spreadsheet. But if you spend enough time inside actual investment decisions, you learn that those harder things do most of the work. The yes or no from our side rarely comes down merely to terms.

Every deal is also a public statement. We post about new deals on LinkedIn, the data is published in funding reports, and we get tagged in funding announcements. Other VCs see who we backed. Founders see who we backed. LPs see who we backed. And all of this public performance can impact future calculations. When I'm in a partner meeting, I'm not only asking whether this company will return the fund, I’m also asking whether we want to be associated with them in public. In other words, whether their reputation will positively reflect on ours in three years time, when the founder community is comparing notes on how they treated their employees, their co-founders, and their early investors.

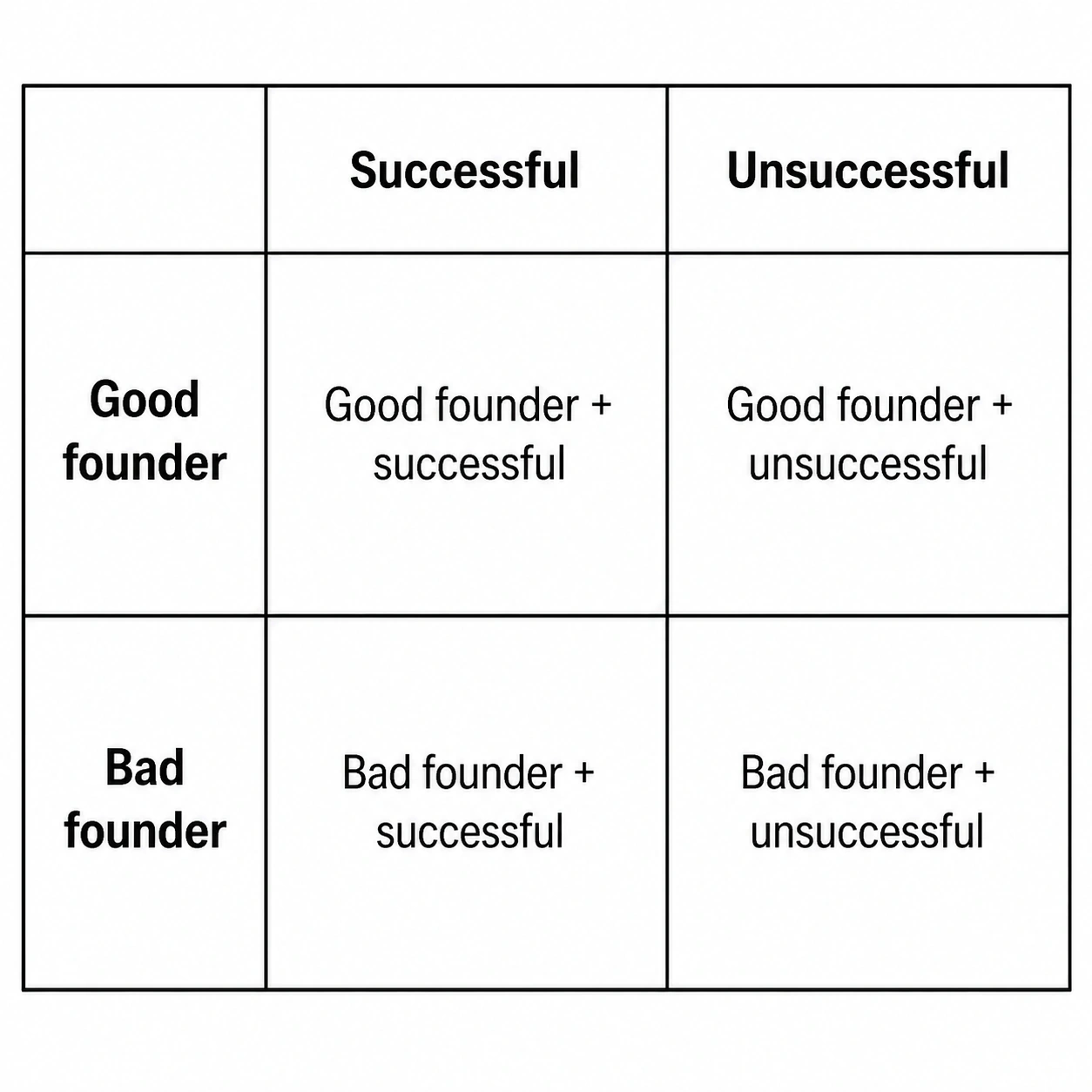

This is why, personally, I think it's better to back a ‘good founder’ who doesn't get an outcome straight away than a bad founder who does. There's a simple matrix you can sketch on the back of a napkin for each individual deal:

At my stage of investment, I'd rather sit across the top row of that matrix… even if it sometimes costs us a short-term hit. Why? Because the reputation damage from being associated with bad actors - even if they succeed - is real, and its effects last longer than IRR (Internal Rate of Return).

If you're a founder, then make this the one thing you take away from reading this: investors are making a public bet on you. Your community is watching how you negotiate, while future co-investors and acquirers and employees are forming an opinion of you in this exact phase of your growth.

The ‘Founder Archetype’ VCs actually want to back

Character usually shows up in how a founder manages their network. When my partners and I are making a final decision, the conversation more often than not lands on questions like: will this person engage with our support, or just cash the check? Will they help other founders in our portfolio? Are they generous with people, or do they burn through them? Slash-and-burn founders might go fast, but in my experience they don't tend to go far. People who cultivate their networks and manage them responsibly are giving off a soft signal about whether they can build something durable, as well as how they manage uncertainty and stressful situations. At early stages, these signals do more work than any deck ever can.

This is where the Midwest version of what I’m trying to articulate may get uncomfortable for some, so I'll just say it. I see plenty of deals from outside the region including from the Bay Area, LA, Austin and New York. When I work with founders from those cities, I don't have to do nearly as much explaining as I do here. That's just a fact about ecosystem maturity. Coastal founders already know the language of venture. They know what a cap is, what pro rata means, what participation does. When they push back on terms, they're pushing back with information.

Here, a lot of the friction is down to knowledge. Founders pick up terminology they don't fully own, get burned once, and decide the whole system is rigged. Let’s be real for a minute and say that there are genuinely some bad actors out there in the investor space. But some of the issues founders feel are their own knowledge gaps, and this gap creates an adversarial default. The first time a Midwest founder walks into a venture conversation, they often expect to get screwed. So they fight for control over things that aren’t important to us, and therefore miss what the investor across the table might actually be offering.

But our local advantage is also different to those elsewhere in the country. When we invest in a local founder, we have real leverage to be useful: opening doors, pulling in our portfolio for advice, giving them something other than ‘only’ money. Coastal founders backed by huge coastal funds usually take the wire and never see the partner again. The investor doesn't have the time. The founder doesn't necessarily expect it. These are more transactional markets by their very nature, and often produce more transactional founders for these reasons. But we don't HAVE to copy that posture here, and in my view we probably shouldn't.

A friend of mine likes to say “would you rather have a slice of a grape or a slice of a watermelon?” It's a clichéd line, but is also the right question for any founder who is over-indexing on their cap table. I'm not telling founders to give up control for the sake of it. I'm telling them that capital is the cost of entry. The prize is the company you build, the network you cultivate, and the reputation you earn over the next decade. Most founders who succeed eventually figure out how to make every conversation about more than ‘just’ money. The ones who don't — the ones who keep dragging every meeting back to who has the bigger number on the page — tend to win an argument but eventually lose a company.

Money is the simplest thing in that room. Treat it that way. THEN go and figure out what else you can win.

The Secret VC is a genuine and experienced investor, based here in the Midwest. They will remain anonymous as long as they choose to, so please don't ask us who they are. The goal here is to inform, and share some home truths while we're at it. If you'd like to submit a topic or questions to be covered by The Secret VC, then go ahead and contact us here.

Read more on this topic

Latest Videos

All Rights Reserved

Copyright 2026 Zeroto7 LLC

Powered by: